To try and create greater familiarity for those living elsewhere, we’ll periodically profile some China brands and businesses that we believe will be household names across the world soon. This month let’s look at Huazhu Hotels , a silent giant in the hotel category in China.

The Huazhu Group has several brands, well over a thousand properties in China, a strategic alliance with Accor and acquired a German hotel group called Deutsche Hospitality in late 2019. They’re listed on NASDAQ under HTHT.

Background

Ji Qi ( 季琦) the founder, apparently got the idea to start the chain when he read a book about the Accor Hotels group. Interestingly for the founder, the group that inspired him eventually had a strategic alliance with HuaZhu from 2016 although recent reports suggest that Accor has now started to divest their shareholding in the group given it’s focus on budget and mid-price hotels rather than luxury.

The company brands include Hanting Inns and Hotels (汉庭连锁酒店; 漢庭連鎖酒店; Hàntíng Liánsuǒ Jiǔdiàn) including Hanting Express (汉庭快捷; 漢庭快捷; Hàntíng Kuàijié); Hi Inn (海友酒店; Hǎiyǒu Jiǔdiàn); JI Hotel (全季酒店; Quánjì Jiǔdiàn), Starway Hotel (星程酒店; Xīngchéng Jiǔdiàn), Joya Hotel (禧玥酒店; Xǐyuè Jiǔdiàn), and Manxin Hotels and Resorts (漫心度假酒店; Mànxīn Dùjià Jiǔdiàn). The company classifies Joya and Manxin as upscale brands, JI and Starway as midscale, and Hanting and Hi Inn as economy brands. The most casual traveler to China will start seeing these hotels right as they leave the airport or train station in any city – low cost and ubiquity are key to the success of the business.

Financials

Huazhu Group is listed on the NYSE and publishes annual reports, so it’s easy to track their financial performance. After steady growth in revenue and profit from 2017 all the way until 2019, when they finished up with about 11 billion RMB in revenue and 1.7 billion in profit, they slid to just over 10 billion RMB and a loss of over 2 billion in 2020. Clearly they were hugely hit by the pandemic and called that out as a major factor in their annual report – the fact that their acquisition in Europe was on Jan 2, 2020 would have been unfortunate timing, since the impact on travel there lasted through most of the year. At the same time Accor divested 1.5% of Huazhu shares for $289 million (they continue to have a 3.3% holding) so the company is clearly worth a great deal and should be able to weather the storms of the pandemic, especially as China recovered fairly quickly.

Huazhu is the 3rd largest hotel group in China after Oyo and Jin Jiang Hotels, with 5400 properties against 19,000 and 10,000 for the other two. Jin Jiang is state owned and reported a 32% drop in revenue to about 14 billion RMB in 2020 with 1.68 billion in profit. Oyo is more an aggregator than a hotel chain with its own properties. Huazhu has the wherewithal to overtake the other two, especially as Oyo is still loss-making after 8 years of existence.

Success Factors

The two strategies clearly in favor of the group are ubiquity and a focus on the budget / mid-priced segment. While they do claim to own two “premium” brands, those are not the focus and they’ve successfully captured the budget travel market across China. Their acquisition in Europe seems to be based on the same approach and while that seems to have caused some change of heart at Accor, Huazhu will very likely continue with M&A to extend its vision for affordable accommodation across the rest of the world.

Future Outlook

The significant loss in 2020 is somewhat surprising given that China bounced back from COVID by mid-year. If Huazhu is able to overcome that setback in 2021 and beyond it should be well-poised to continue its expansion outside China.

While our focus as a consultancy is making new brands famous in China, there are many (already) famous Chinese brands that aren’t well known overseas. We will be bringing them to light in this series over time.

If you’d like your brand to be famous and successful in China reach out to us at enquiries@searchlightchina.com – we work with both local startups as well as international brands that would like to do better in this market.

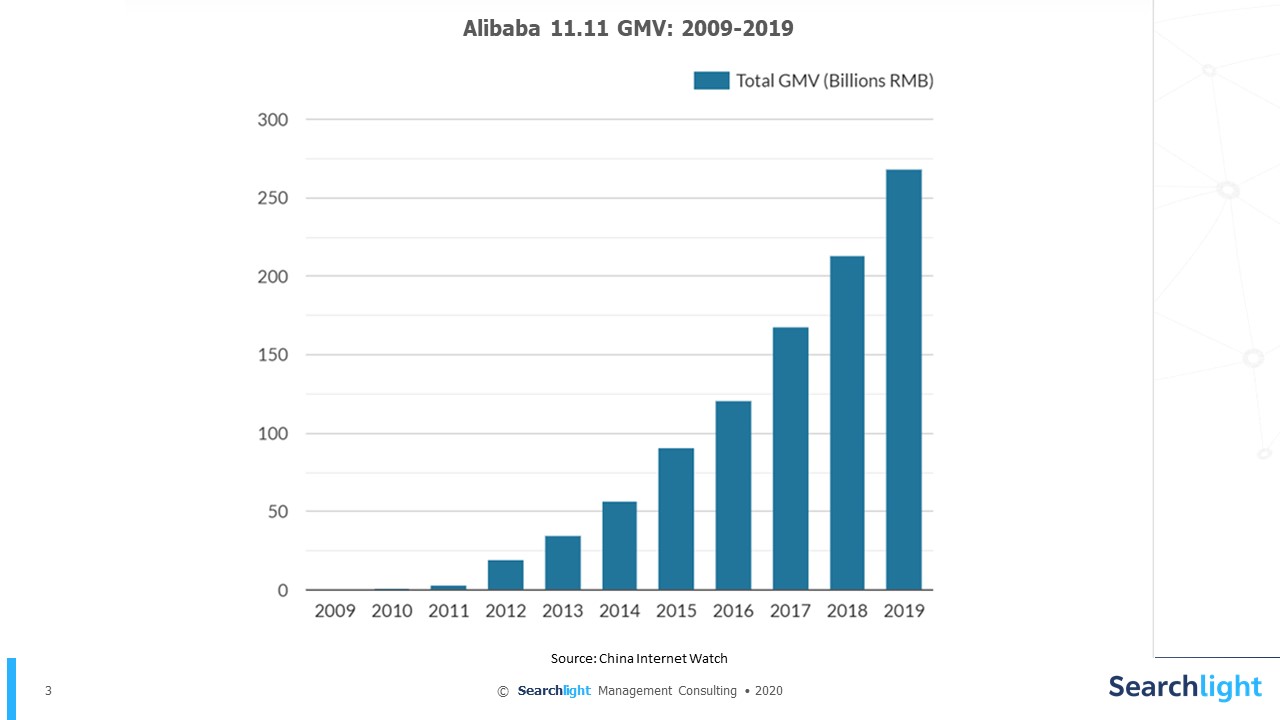

It’s interesting to look back at 2009 when this took place for the first time and note that only 27 brands took part in a one-day sale that netted about 50 million RMB in GMV. That number has grown exponentially to 268 billion RMB in 2019. More than 100 brands rang up sales of over 15 million USD (about 100 million RMB) in the first two hours of that day – each more than double the value of that first 11.11 more than a decade ago.

It’s interesting to look back at 2009 when this took place for the first time and note that only 27 brands took part in a one-day sale that netted about 50 million RMB in GMV. That number has grown exponentially to 268 billion RMB in 2019. More than 100 brands rang up sales of over 15 million USD (about 100 million RMB) in the first two hours of that day – each more than double the value of that first 11.11 more than a decade ago.